Trust accounting rules for law firms sit at the very heart of professional compliance in the UK. Breach them — even accidentally — and you face SRA intervention, financial penalties, or suspension. In the most serious cases, the SRA will strike off the firm entirely. As a law firm manager, you must understand these rules. They are not optional.

Yet the SRA Accounts Rules 2019 remain one of the most misunderstood areas of practice management. The terminology is precise. The obligations are exacting. The margin for error is narrow.

So, in this guide, we break down every essential trust accounting obligation for managers of law firms in England and Wales. We keep it clear, practical, and free from unnecessary jargon.

Trust accounting covers how your firm handles money that belongs to clients or third parties. This money differs legally from your firm’s own funds. Consequently, you must keep it in a separate account, track every penny, and return or apply it only when your client instructs you to do so.

In England and Wales, the SRA Accounts Rules 2019 govern all client money. These rules replaced the earlier 2011 version. Importantly, the current rules follow a principles-based approach rather than a prescriptive one. This gives firms more flexibility — but it also puts greater responsibility on managers to build and maintain solid internal controls.

Therefore, understanding the spirit of the rules matters just as much as knowing the letter of them.

The foundational principle of trust accounting is segregation. You must hold client money in a dedicated client account — a bank account in your firm’s name, clearly designated as a client account. Moreover, you must never mix it with your firm’s own money.

Client money includes the following:

By contrast, certain funds do not count as client money. For example, payments settling an already-delivered and agreed bill fall into office money. Similarly, payments for disbursements your firm has already incurred and invoiced sit in the same category. Misclassifying one type as the other is a compliance error — and it carries real consequences.

Warning: Paying the firm’s own invoices or expenses from the client account — even temporarily — breaches the SRA Accounts Rules. This holds true regardless of your intent.

Under Rule 2, your firm must return client money promptly once you no longer need to hold it. In practice, this requires active monitoring of client balances. Dormant balances — funds sitting in the client account with no live matter attached — are a red flag for the SRA. They also present a risk management problem for your firm.

To address this, ensure your fee earners confirm at matter closure that all client monies are accounted for. At that point, either return the funds or transfer them legitimately to your office account.

Only client money may go into a client account. The SRA does permit a small amount of firm money to cover bank charges, but you must keep this to a minimum and record it accurately.

Furthermore, your firm may only withdraw money from the client account in defined circumstances:

Withdrawing client money for any other reason — for instance, to cover a short-term cash flow gap in your office account — is a serious breach. Even borrowing the funds temporarily does not make it acceptable.

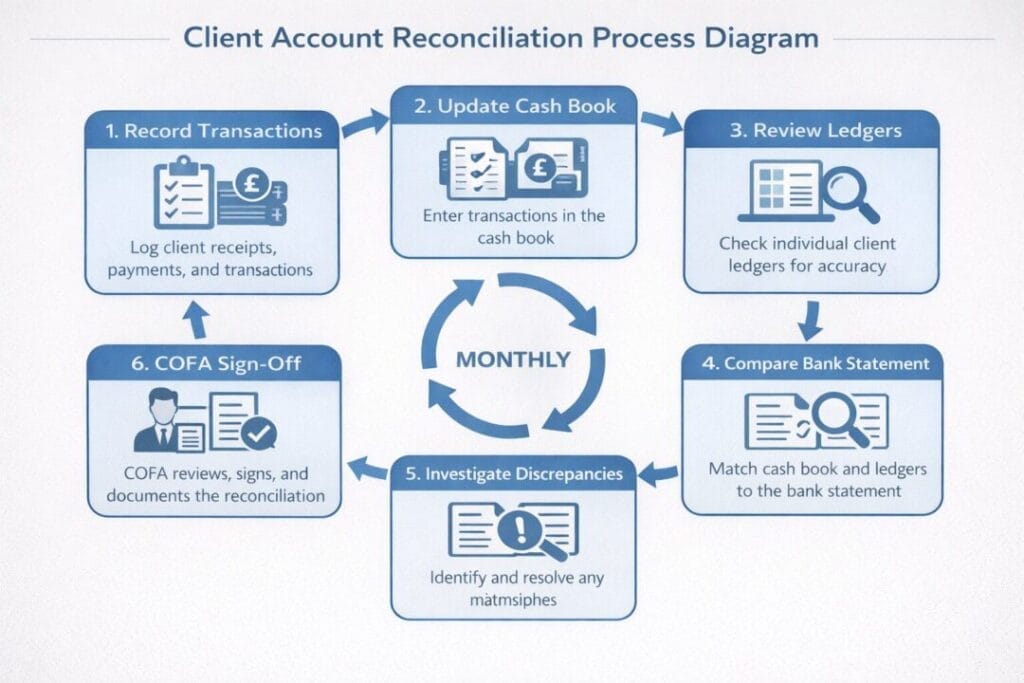

Reconciliation is the operational cornerstone of trust account compliance. Specifically, your firm must reconcile its client account at least every five weeks. During this process, you must compare three figures:

All three figures must match. If they do not, investigate the discrepancy immediately. Furthermore, do not leave any difference unresolved — even a minor one. Leaving gaps on a reconciliation statement, however small, signals poor financial controls.

Firms that use legal accounting software to automate their reconciliation process significantly reduce the risk of undetected discrepancies building up over time.

Every SRA-regulated firm must appoint a Compliance Officer for Finance and Administration — the COFA. This individual carries personal regulatory responsibility for the firm’s compliance with the Accounts Rules. You can read the full scope of those duties in the SRA’s guidance on COFA responsibilities, and the Law Society’s practice note on compliance officers provides useful supplementary guidance for firms of all sizes.

In small firms, the COFA is often the practice manager, a senior partner, or an experienced legal cashier. Regardless of the structure, the responsibilities stay the same:

Importantly, the COFA role is not ceremonial. The SRA has taken enforcement action against individual COFAs where inadequate oversight allowed systemic accounting failures to develop undetected over time.

Understanding where firms most often breach the Accounts Rules helps you build targeted controls. Below are the five most frequent categories the SRA identifies during investigations.

This is the most common finding. Firms either let reconciliations run overdue or complete them on paper without investigating differences. To prevent this, set a mandatory reconciliation date inside your practice management system. Better still, use legal process automation tools to schedule and trigger reconciliation workflows automatically, so no deadline slips through.

Small balances linger on client ledgers after matters conclude. Over time, they accumulate and create both a compliance risk and a potential liability. To address this, run a monthly residual balance report and require fee earners to resolve any balance above your de minimis threshold within thirty days of matter closure.

Some firms transfer money from the client account to the office account before delivering a bill. Even where the client agrees verbally, this still constitutes a breach. The rule requires a written bill or written cost notification before any transfer can lawfully proceed.

Receiving client payments into your office account — or office income into your client account — creates an immediate breach. Consequently, training all fee earners and support staff to identify incoming payments correctly is essential. One poorly labelled receipt can trigger a compliance investigation.

Holding client money longer than necessary exposes your firm to regulatory scrutiny. Whether the delay results from administrative oversight or workflow bottlenecks, the SRA treats it seriously. Therefore, document your turnaround standards for paying disbursements, completing transactions, and returning surplus funds — and enforce them.

Note: SRA investigations frequently begin with a routine inspection of client account reconciliations. A firm that cannot produce accurate, up-to-date records faces a significantly elevated risk of formal regulatory action.

When your firm holds client money in a client account and that money earns interest, you must account to the client for a fair and reasonable sum. The SRA no longer prescribes a specific rate. Instead, your firm must maintain a written interest policy and apply it consistently across all clients.

In practice, this means doing the following:

Beyond the regulatory obligation, failing to pay interest can expose your firm to civil claims. Clients deprived of money owed to them have grounds to pursue recovery, sometimes with additional costs.

Manual trust accounting — spreadsheets, paper ledgers, standalone cashbooks — is not only inefficient. It also introduces compliance risk. Human error, delayed reconciliations, and limited visibility into client balances are precisely the conditions that lead to the kinds of breaches the SRA investigates.

By contrast, integrated legal accounting software eliminates many of these risks. Specifically, good software will do the following for your firm:

Billing-to-transfer integration: Transfers from client to office account link automatically to the corresponding bill. Combining trust accounting with your firm’s broader software integrations — such as HMRC for SDLT, Xero for accounting, and DocuSign for e-signatures — ensures that every step of the transaction chain connects cleanly, reducing the risk of errors at handover points.

SpineLegal’s trust accounting module is purpose-built around the SRA Accounts Rules 2019. It includes automated reconciliation scheduling, COFA sign-off workflows, and residual balance monitoring as standard — so compliance becomes part of your daily workflow, not a separate exercise.

The SRA requires your firm to keep accurate accounting records that allow you to establish your firm’s financial position at any point. Specifically, you must maintain the following:

Crucially, these records must be available for SRA inspection at any time and without advance notice. Firms that fail to produce accurate records on request face immediate risk of regulatory intervention.

A client account holds money that belongs to your clients or third parties. An office account holds your firm’s own money — income, expenses, and profit. You must never mix the two. Moreover, you must pay any client money you receive into the client account on the day of receipt, or by the next working day at the latest.

Under Rule 8 of the SRA Accounts Rules 2019, you must reconcile your client account at least every five weeks. However, many well-managed firms do this monthly or more frequently — particularly where transaction volumes are high. After each reconciliation, the COFA must review and approve the output.

The outcome depends on the severity of the breach. Minor, self-reported, and promptly resolved breaches may result in a corrective action requirement and enhanced monitoring. However, serious or systematic breaches — especially those involving misuse of client funds — can lead to intervention, suspension of your firm’s authorisation, financial penalties, and referral to the Solicitors Disciplinary Tribunal. Furthermore, individual fee earners and the COFA may each face personal sanctions.

Start by reviewing your current pain points: manual reconciliations, residual balance backlogs, or billing transfer errors are the most common triggers. Then evaluate platforms on the basis of SRA Accounts Rules alignment, automated reconciliation capability, COFA workflow support, and integration with your existing tools. Our guide on choosing legal software for your firm sets out the key criteria to assess before committing to a platform.

The SpineLegal practice management platform is built specifically for UK law firms. Our platform includes a fully integrated trust accounting and client ledger module that aligns with the SRA Accounts Rules 2019 — helping small and mid-size firms maintain compliance without the administrative burden of manual processes. To learn more or to book a demonstration, visit our website or contact our team directly.